As September begins, the price wars and traffic battles of the “Golden September, Silver October” sales season are about to commence.

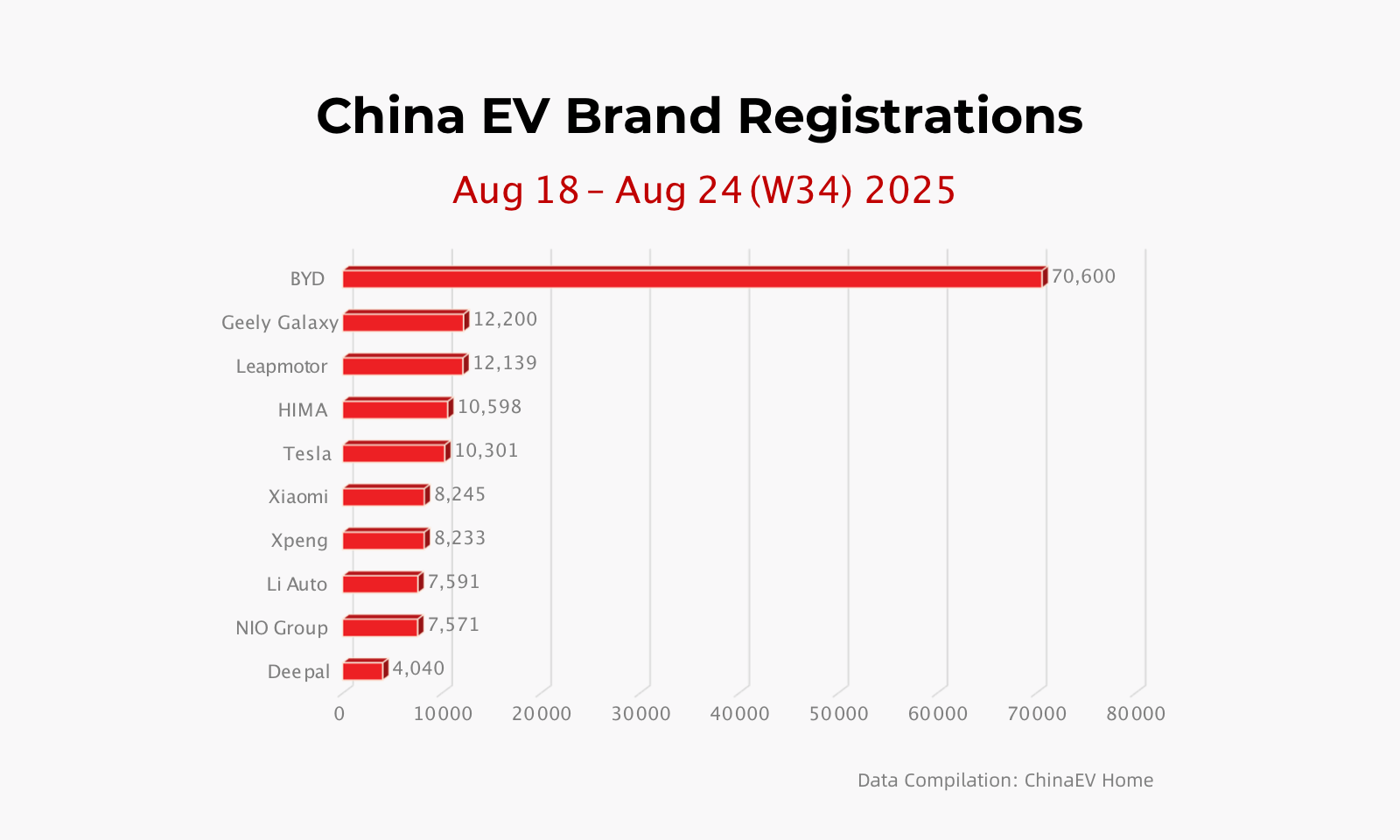

There were significant changes in this week’s sales rankings. BYD secured the top spot with a commanding lead, selling 70,600 units, an 8.3% increase week-on-week.

Reportedly, since August, BYD’s Shenzhen and Changsha plants have implemented a “double-shift” system, increasing daily production capacity to 7,500 units. It is worth mentioning that despite BYD narrowing its terminal discounts, sales were not significantly affected, demonstrating strong brand demand.

ChinaEVHome

ChinaEVHome

Tesla, originally in second place, fell to fifth with sales of 10,300 units, a 26.42% decrease week-on-week.

During the statistical week, the Model Y L, launched by Tesla specifically for the Chinese market, officially went on sale with a starting price of 339,000 RMB ($47,200). The model garnered roughly 35,000 orders on its first day, a figure that will influence the sales rankings in the weeks ahead.

ChinaEVHome

It is worth noting that sales of new energy vehicle startups all showed an upward trend.

Leapmotor maintained strong market performance, securing third place with sales of 12,139 vehicles, a 16.77% increase week-on-week. This marks the fourth consecutive week in August that Leapmotor has been the weekly sales champion among new automaker brands.

ChinaEVHome

Following closely, HIMA ranked fourth with 10,600 units. The AITO brand remains the main sales contributor to the Harmony family, with the AITO M8 again exceeding 5,000 units, firmly holding the top spot in large SUV sales for the week. Its sibling model, the AITO M9, sold 2,589 units.

On August 25th, HIMA, alongside its four brands, simultaneously launched multiple new models, including the all-new LUXEED R7/S7, the AITO M7 pure electric version, and the Shangjie H5.

With the start of deliveries for the first vehicle from the Shangjie brand, which targets the mainstream family market, Harmony Intelligence’s overall sales have an opportunity to reach a new level.

As of August 25th, cumulative deliveries for Harmony Intelligence have reached 900,000 units.

ChinaEVHome

NIO Inc. maintained stable growth with weekly sales of 7,570 units, a 5.4% increase week-on-week. This includes 2,584 units for the NIO brand, 4,104 units for the ONVO brand, and 883 units for the Firefly brand. Since the launch of the ONVO L90, ONVO’s market exposure has been steadily increasing, with weekly sales reaching 2,542 units, making it the new main sales driver.

ChinaEVHome

Xiaomi Auto performed notably well this week, with sales of 8,245 units, moving up two places in the overall ranking. This includes 4,346 units of the Xiaomi SU7 and 3,899 units of the Xiaomi YU7. Cumulative deliveries of the Xiaomi YU7 are about to surpass 20,000 units.

It is worth mentioning that after the Phase II plant in Beijing E-Town commenced operations in August, daily production capacity has climbed to 1,000 vehicles. However, system displays still show a waiting period of 12-14 weeks, indicating that a large number of orders still face “delivery” challenges.

Li Auto sold 7,600 units, maintaining sales growth for two consecutive weeks. With the commencement of large-scale deliveries of the Li i8, sales may see new breakthroughs later on.

ChinaEVHome

Underlying currents surge beneath the Week 34 data. BYD remains firmly entrenched as the weekly sales leader. NIO and XPeng have successively launched new models, using product release rhythms to achieve “off-peak harvesting.” AITO continues to increase volume, competing with Li Auto in the extended-range segment.

As September begins, the price wars and traffic battles of the “Golden September, Silver October” sales season are about to commence.

Discover more from ChinaEVHome

Subscribe to get the latest posts sent to your email.