Sales data for Week 28 was released, where Tesla witnessed a sharp rebound in deliveries.

For the 28th week of 2025 (July 7–13), sales data from leading Chinese new energy vehicle (NEV) startups and brands show a largely stable competitive landscape, though some brands experienced notable fluctuations in delivery volume.

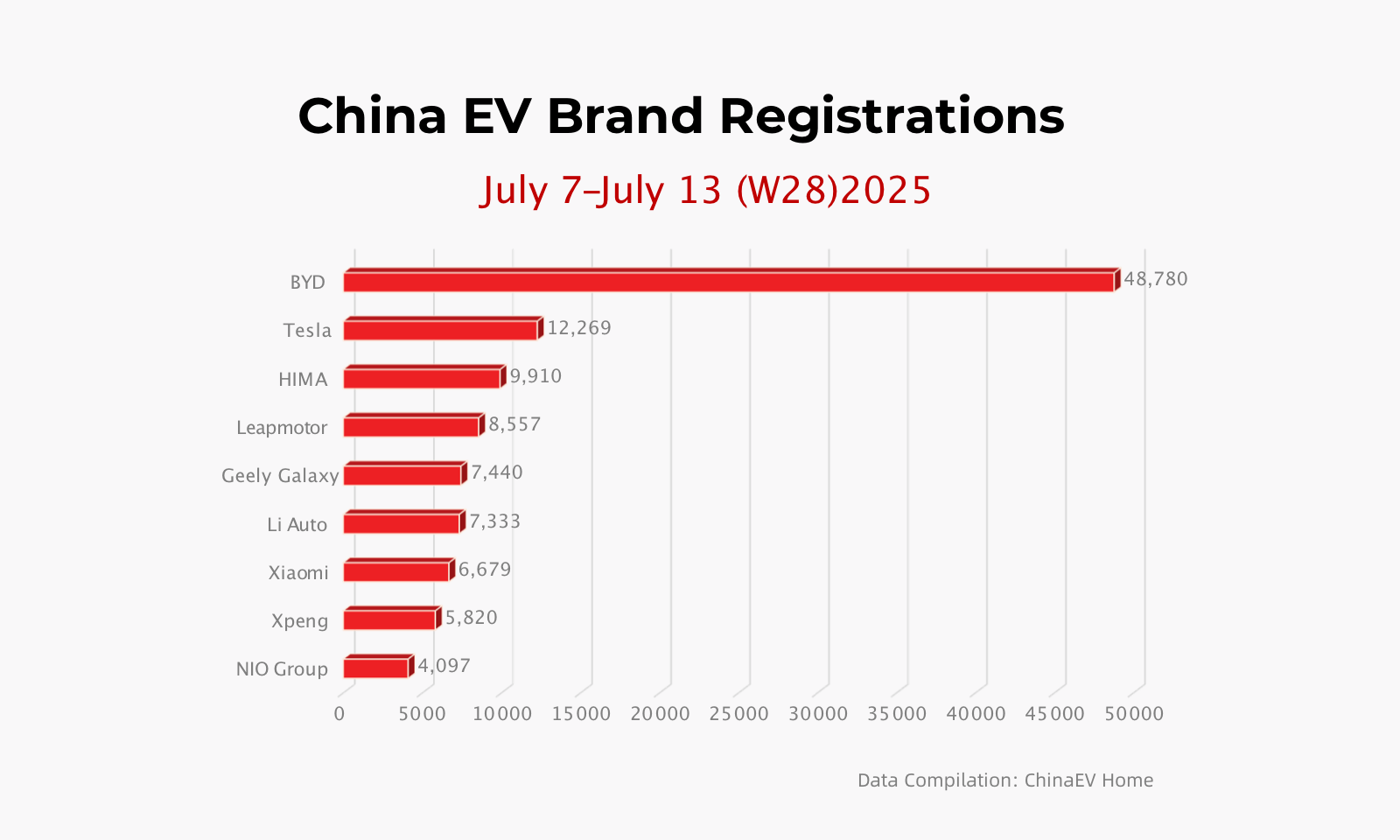

Tesla, with 12,269 vehicles delivered in China, marked a sharp 145% rebound from the previous week’s dip (5,006 units). The surge was partly driven by inventory clearance cycles and adjustments in domestic and export delivery scheduling.

Harmony Intelligence Mobility Alliance (HIMA) jointly delivered 9,910 units—an 11.4% decline from the 11,187 units in Week 27. Among them, AITO delivered 8,610 units (down 8.4% week-over-week), while LUXEED and STELATO posted 940 and 330 units respectively, down 25.1% and 31.5%. Newly-launched premium brand MAEXTRO appeared in the rankings for the first time, with 31 units delivered.

Leapmotor maintained steady performance, delivering 8,557 units—virtually flat from last week (down 0.3%). Li Auto reported slight growth with 7,333 units delivered, a 2.4% week-over-week increase. Xiaomi continued its upward momentum, delivering 6,679 units, a 36.6% increase as SU7 production ramp-up and dealership expansion progressed.

XPeng delivered 5,820 units, down 9.8% from the prior week. Zeekr, NIO, and Denza showed relatively stable performance with minor fluctuations between 5% and 7%. Notably, NIO Group (including NIO, ONVO, and Firefly) delivered a combined 4,097 units, down 19.6% week-over-week. Within the group, the core NIO brand accounted for 2,412 units, continuing to serve as the group’s volume anchor, followed by ONVO (1,133 units) and Firefly (552 units).

Looking at the broader trend, while a few brands posted week-over-week gains, most NEV startups appeared to enter a brief adjustment or observation phase. This is likely tied to model transitions, promotional cycles, and customers awaiting new model launches during the summer.

As mid-July approaches, the leaderboard suggests an emerging reshuffle. Tesla is benefiting from a post-supply chain rebound, while brands like AITO, Leapmotor, and XPeng may experience short-term volatility. With summer promotions kicking off and a wave of new models set for delivery, competition in Q3 is poised to intensify further.

Discover more from ChinaEVHome

Subscribe to get the latest posts sent to your email.